What Is Predictable Income Investing?

Predictable income investing is a financial management strategy that focuses on building a portfolio of assets which pay you a regular, dependable cash flow. Instead of aiming for big capital gains, you invest in things like bonds, dividend stocks, and annuities that consistently pay interest or dividends. These are often called fixed-income investments – Investopedia notes they pay fixed periodic interest and return your principal. This approach can suit anyone who needs steady cash from their savings.

Why Predictable Income Matters

Having a reliable income stream brings peace of mind, especially in retirement or volatile markets. If you know your investments will pay a set amount each month or year, you’re less likely to panic-sell when stock prices dip. Advisors point out that predictable income is “invaluable” for retirees, since it “helps retirees maintain their standard of living without the stress of market fluctuations”. In practice, having some guaranteed payouts (like annuities or bond interest) means you can cover essential expenses even when markets fall.

Common Income-Generating Investments

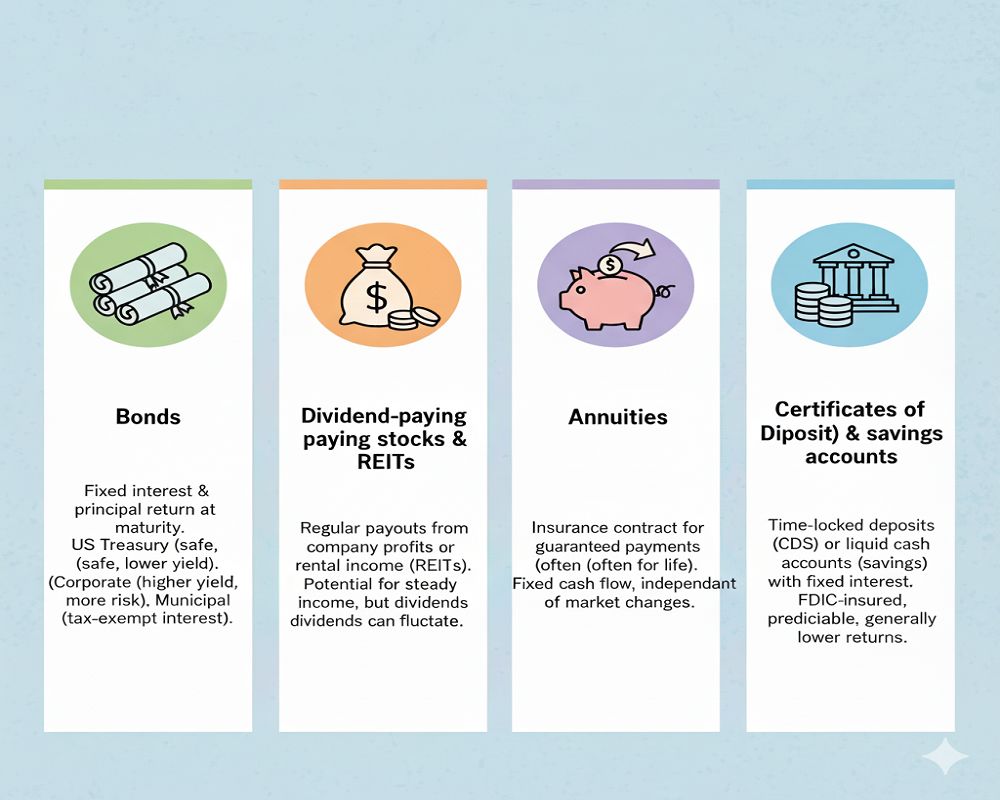

Bonds (government, corporate, municipal): Bonds pay fixed interest and return your principal at maturity. U.S. Treasury bonds (government loans) are very safe, while corporate bonds usually pay higher yields with more risk. Municipal bonds (state or local loans) also pay interest that is typically exempt from federal (and sometimes state) taxes.

Dividend-paying stocks & REITs: Many established companies pay regular dividends from their profits, providing ongoing income. Real Estate Investment Trusts (REITs) own rental properties or mortgages and by law must distribute most of their income as dividends. Both can offer steady payouts, though dividends can be cut if earnings fall.

Annuities: These insurance contracts convert a lump sum into guaranteed payments (often for life). An annuity acts like a private pension: once payments start, they generally don’t change, ensuring a fixed cash flow regardless of market swings.

Certificates of Deposit (CDs) & savings accounts: Bank CDs lock your money for a set term at a fixed interest rate. High-yield savings accounts offer higher interest on cash balances. Both are FDIC-insured and provide predictable (though usually lower) returns.

Strategies for Building Predictable Income

Bond laddering: Buy bonds (or CDs) that mature at different times. When one bond matures, you reinvest it in a new long-term bond. Schwab explains a ladder can help “structure monthly bond income,” smoothing out changes in interest rates.

Cash/maturity buckets: Keep a portion of your portfolio in short-term safe assets (cash, money market funds, or short bonds) for near-term expenses. Invest the rest in longer-term income assets. This ensures you have money ready to spend without selling long-term investments during a downturn.

Tax-aware placement: Place income-generating assets strategically. For example, hold taxable bonds or CDs in tax-deferred accounts (IRAs, 401(k)s) to defer taxes, and use tax-free assets (like muni bonds) in taxable accounts. This can boost your after-tax income.

Risks of Predictable Income Investing

Interest rate & inflation risk: If market interest rates rise, the prices of existing fixed-rate bonds fall. Also, high inflation can erode the purchasing power of fixed payouts over time. (As Investopedia notes, fixed-income investments face risks like “inflation, interest rate changes, and credit risk”.)

Credit/default risk: Your income depends on the issuer’s health. U.S. Treasuries have virtually no default risk, but corporate bonds or some annuities can fail to pay. Some bonds are callable (redeemed early by the issuer), which forces reinvestment at a lower rate.

Dividend risk: Companies can reduce or eliminate dividend payments if profits drop, so income from stocks is not guaranteed.

Conclusion

Predictable income investing trades some growth potential for stability and peace of mind. By building a mix of bonds, dividend stocks, and other income vehicles, you create a more reliable “paycheck” from your portfolio. This approach is especially useful if you depend on your investments to cover living expenses. Within the broader context of financial management, this strategy helps balance risk and reward while maintaining cash flow. However, focusing too much on income can limit growth and may not keep up with inflation. As one guide notes, achieving a steady income stream is “essential for financial stability.” Most advisors recommend combining steady-income investments with some growth assets to suit your long-term goals.

Read our latest blog posts for more information.